Reasons Why Market Could Be Overly Pessimistic on China

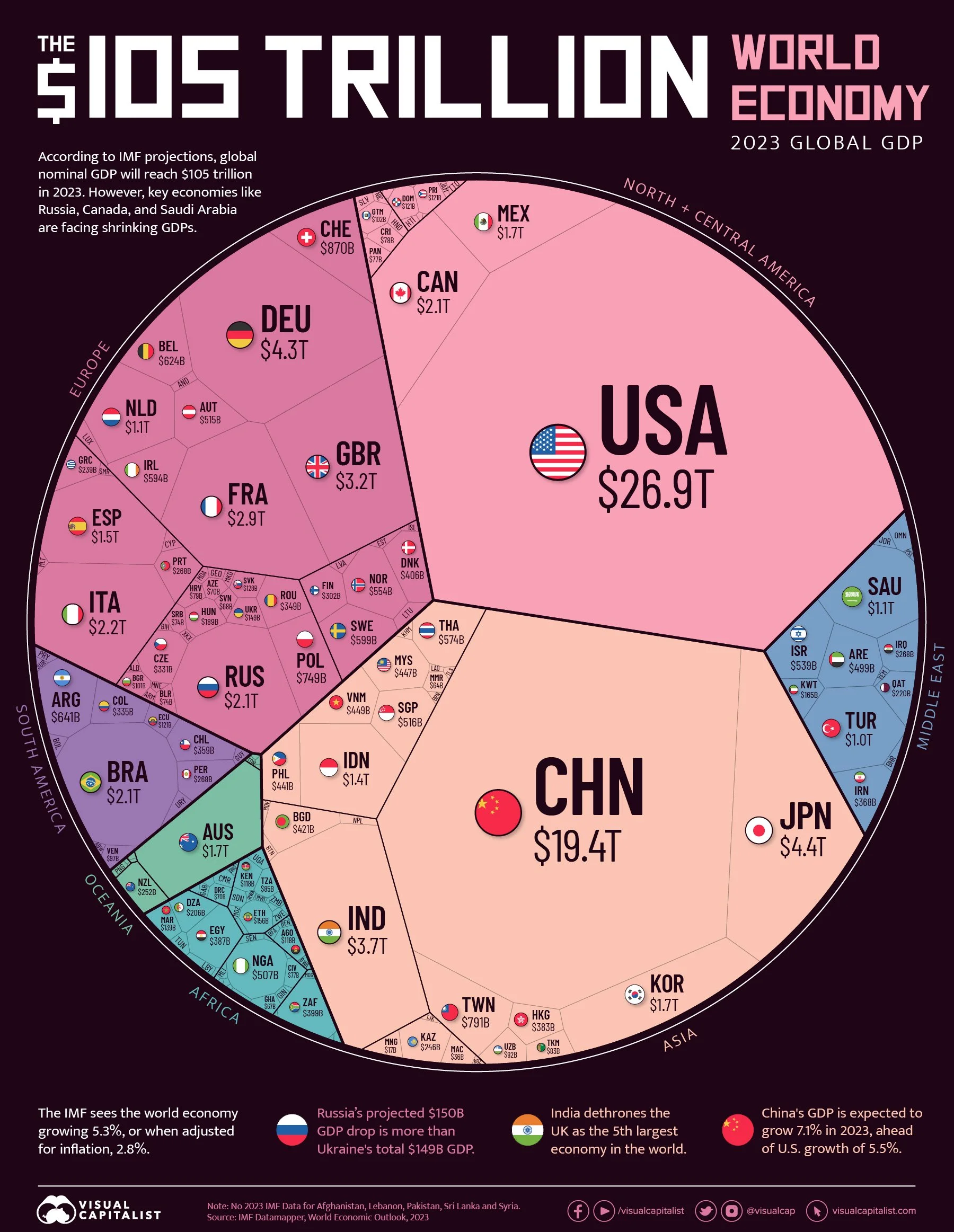

Neglecting Chinese Economy Sheer Size: The Chinese economy is impressive despite its challenges. Barclays cut its forecast for China's 2023 GDP growth to 4.5%. Even at a 3% annual GDP growth rate over a decade from now, China’s economy would still grow by the equivalent of approximately two times the 2022 GDP of India. Please refer to the 2023 World Nominal GDP data visualization below.

Off-Cycle COVID Response Is The Culprit For Recent Headlines: While most OECD countries moved past the harshest impacts of COVID two years prior, China's final wave started this January, impacting consumer confidence and spending. Nonetheless, with each passing month, the expectation is that the confidence of Chinese consumers will rebound, underpinned by their considerable savings and steady income growth.

Possibly Overrated Current Structural Challenges:

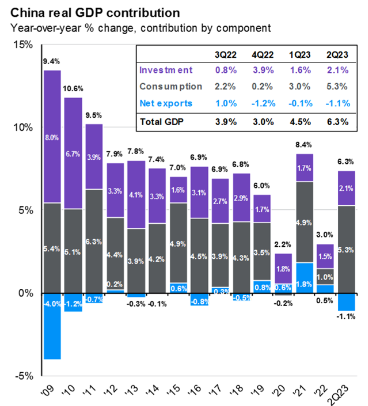

Deflation: China's Consumer Price Index (CPI) is low compared to peers, but deflation is not imminent. The drop in CPI is mainly attributed to a sharp decline in global oil prices and pork prices. We can see from JPM’s Guide below that consumption in % of real GDP YOY growth has almost never dipped below zero, with the exception of 2020 by -0.2% due to lockdown under pandemic measures.

Youth Unemployment: There's a rise in unemployment among urban youth, especially recent college graduates due to weak industrial activity and slow job recovery post-zero-COVID. While high unemployment is concerning for this educated elite group, their restrained response(they are unlikely to protest so as to not jeopardize future employment prospects) and government initiatives(state agencies and SOEs are now encouraged to hire more young people,) and continued recovery in services jobs to boost hiring can potentially alleviate this issue and support economic recovery. China still has the highest number of engineers and STEM graduates in the world and they are a tremendous asset and a competitive advantage when AI is playing an increasingly important role in improving productivity. Given the seismic demographic structural shift into an aging society, under which the global work workforce is dwindling, I am convinced that youth unemployment is a short-term problem for China since she will have to develop talents internally rather than resort to the short-term solution of immigration since:

Per-capita GDP is still developing nation level(despite unprecedented growth in total GDP since the 2000s) and has lower HDI and quality of life compared to those of developed countries,

Mandarin, even a simplified version, is still a hieroglyphic language that is tremendously difficult for non-Chinese audiences to command, at a professional level(to write especially), compared to languages that underwent Transliteration(i.e. Japan’s Furigana and Korea’s Hunminjeongeum), or adopted English(i.e. Singapore)

Monochronic and collectivistic cultures emphasize the interests of the community over those of individuals. The predilection of stability over growth has been deeply ingrained into Chinese social fabric. This approach, a legacy shaped by the challenges of harsh geopolitical and climatic conditions, has preserved ancient Chinese civilizations for thousands of years. However, this focus can come at the expense of pursuing individual interests and stifling creativity, making it less appealing to a global talent pool with higher opportunity costs.

Debt Levels: China's debt-to-GDP ratio is high but still manageable(China’s Debt-to-GDP ratio below that of Japan, France, Canada; Q4 2022) Most debts are owed by state-controlled entities to state-controlled banks. Moreover, the overwhelming majority of Chinese debts are denominated in CNY, further lowering the risk of financial crisis or hard landing narratives.

Shift in U.S.-China Relations: The Biden administration's recent reevaluation of its stance on China, as seen through Yellen’s April speech and Blinken’s visit to China, indicates that while political tensions persist, a full-blown crisis seems unlikely. Constructive dialogue can be mutually beneficial. Importantly, China's reliance on exports to the US has diminished compared to a decade ago, meaning strained relations have a reduced impact on China's economic rebound. A complete decoupling between the two is improbable since exports to the US remain significant for China's economy and the US cannot readily absorb a sudden inflationary shock. The US relies on China's manufacturing engine for affordable goods, essential for middle and lower-income groups who will bear the brunt of inflations. In other words, expensive divorce and children's responsibilities will keep the ever-drifting-apart couple together in the foreseeable future.

Domestic Demand: A significant factor often overlooked is China's internal demand, which remains a powerful driver for economic growth. World Bank showed that exports of Goods and Services only consist of 20.7% of Chinese economy in 2022 with an all-time high of 36% in 2006.

Robust Industrial Policy: The industrial sector consists of one-third of the Chinese economy in 2022. Chinese policymakers have proven themselves to be underestimated, pragmatic, and technocratic since Deng’s reform in the late 1970s. China’s dominance in emerging industries like EVs and solar panels is a testament to its forward-looking strategies and their potential for continued economic growth. There have been mistakes made and structural challenges, but Beijing’s track record in generating growth while managing these headwinds has been commendable.

Entrepreneurs Resilience: Despite the two-year regulatory crackdown has suppressed much of the risk appetite of entrepreneurs and consumer confidence, which had contributed to much of the economic woes as 60% of China’s GDP, 70% of its innovative capacity, 80% of urban employment and 90% of new jobs are associated with small and privately-owned companies, Chinese families and entrepreneurs are often proven to be much more resilient than expected. Market timing is extremely difficult to get right. But given how the Chinese policymakers are concerned about bigger economic ramifications, such as higher debt levels, unemployment, and property sector defaults, it is not unrealistic to think that a fiscal stimulus could be under the way, especially when Beijing has ramped up a major campaign and unveiled a “package of reforms” to boost confidence among entrepreneurs in recent weeks.

Chicago, 8/18/2023

Source: JP Morgan - Guide to Market

Source: Visual Capitalist

Updates on 9/1/2023

On my take #6, “is not unrealistic to think that a fiscal stimulus could be under the way” – this just happened.

The structural challenges of Chinese RE sectors will not be solved given the size(25%+ of Chinese economic activities) and industry norm of the pre-sold business model(developers sell the apartments before building and rely on buyers’ mortgage to build rather than their own equity) but these measures will significantly lower the chance of scenario where deteriorating RE, resulted by over-zealous(from hindsight) deleveraging policies in RE sectors, takes down Chinese economy resulting in a hard landing.

Moreover, since Chinese stock markets are too volatile, compared with those of the US, the wealth generated by most Chinese families since 1998 has been stored in residential real estate equity, when President Jiang Zemin’s most crucial housing reform that allowed private sales of real estate properties took place. “At the end of 2019, real estate accounted for 43% of total household assets in China, almost twice the share for U.S. households,” according to a study done by Seafarer. Since most entrepreneurs rely on taking out equity loans against their home equity to support their ventures, a stabilizing RE sector in China will facilitate economic recovery as “60% of China’s GDP, 70% of its innovative capacity, 80% of urban employment and 90% of new jobs are associated with small and privately-owned companies,” according to a HKS study. I think paying close attention to how these recent policies, and potentially future ones as I suspect there are more to come, on the Chinese housing market and measuring their impacts on the broader Chinese economy could pay dividends in thinking about long-term strategic asset allocation and positioning in terms of Chinese exposures.

Updates on 9/28/2023

Regarding my points made in “Shift in U.S.-China Relations” section, Beijing and Washington are working on improving their strained relations, with discussions this week underway for high-level official visits, including a potential summit between Chinese leader Xi Jinping and U.S. President Biden.