Market Observations - August 2023

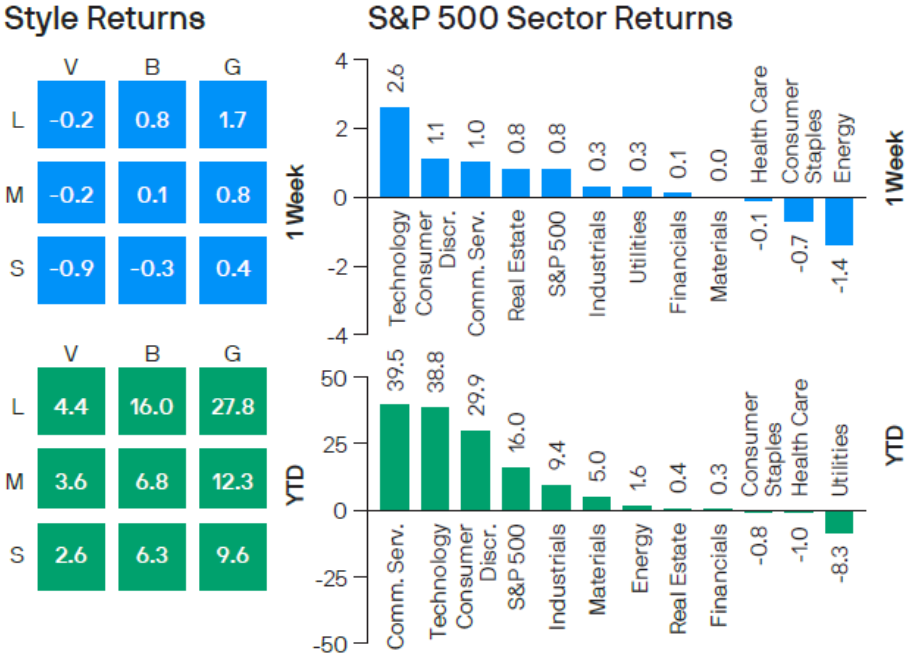

First, let’s recap the returns of styles and sectors:

Source: JPM Market Insights

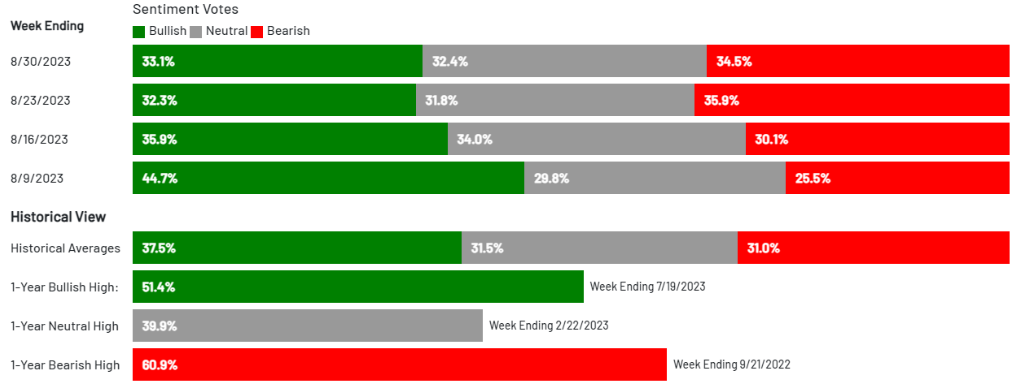

Market sentiment became more bearish in August, surpassing the historical average bearish sentiment of 31%. Given the new labor and consumer confidence data in the last week of August, which supports the soft landing narrative and incentivizes the Fed to suspend rate hikes, bullish sentiment rallied from 32.3% to 33.1%. However, this remains below the historical average of 37.5% for the third consecutive week.

Source: AAII

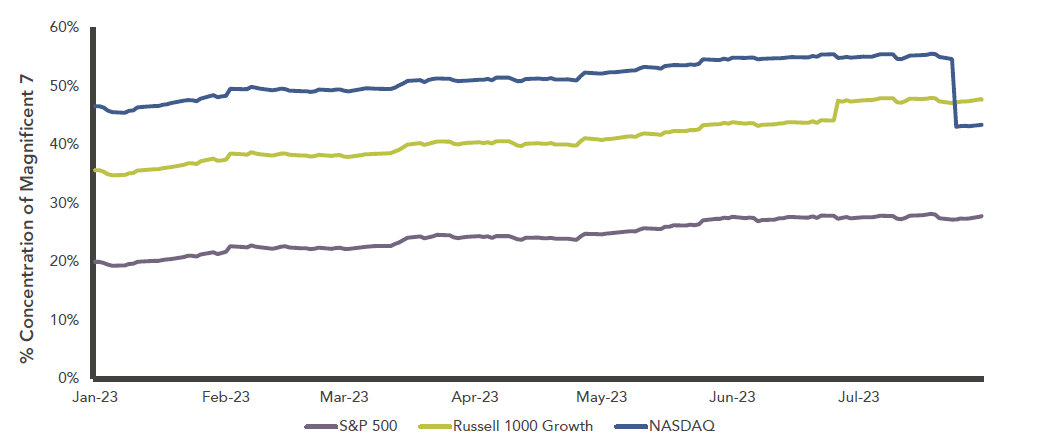

The S&P500 and Nasdaq rebounded from this quarter’s correction, further enhancing their impressive YTD performance. This strong YTD performance is largely credited to the "Magnificent 7," which includes Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Meta. The Magnificent Seven comprises over 40% of the large-cap growth index; NASDAQ underwent a special rebalancing after reaching 55%+ weight of the index.

Source: FactSet as of July 31, 2023. Data visualized by Marquette Associates.

The fundamental market thesis behind the Magnificent 7 is as follows:

AI is presently enhancing the productivity of the US workforce, and these stocks are poised to capitalize on the most significant economic benefits, both through hardware and software. Nvidia's recently reported EPS greatly exceeded even the most optimistic forecasts, suggesting that this trend may persist. We might be in the initial stages of another, possibly the most important, Industrial Revolution that massively increases per capita productivity.

Network effects, combined with a more predictable regulatory environment regarding AI, contribute to higher valuations for the AI sector.

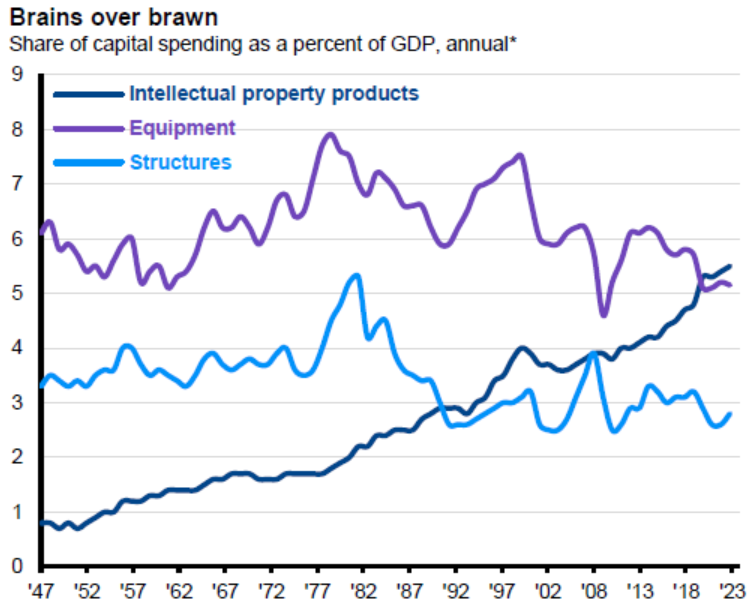

One effect of this thesis is evident by capital expenditures favoring intellectual property spending. Since 2020 this type of investment has been the largest percentage share of GDP for all nonresidential fixed investment components and currently accounts for 5.5% of GDP.

Source: JPM Market Insights

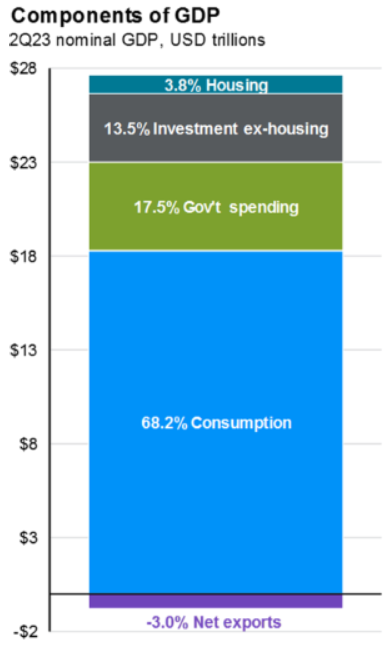

Consumer confidence was measured at 106.1, materially lower than the forecast of 116 and July’s 114.8. This indicator is crucial because 68.2% of US GDP(Q2 2023) comes from consumer spending.

Source: JPM Asset Management

Although this decline supports the soft landing narrative by reducing inflationary pressures, I want to highlight the potential adverse effects of the Fed's efforts to control inflation, given that its decisions are based on ex-post data. Since much of the Fed's information sources are weeks, if not months, out of date relative to current events, the lagging effects of the cumulative impact of higher interest rates could be detrimental. In other words, if the Fed acts too hastily, basing its decisions on lagging economic data, and surpasses the economy's neutral growth rate, the sharp rise in the cost of capital for both consumers and businesses could lead to reduced consumption and capital expenditures. This could risk pushing the economy into recession, stagflation, or even a crisis.

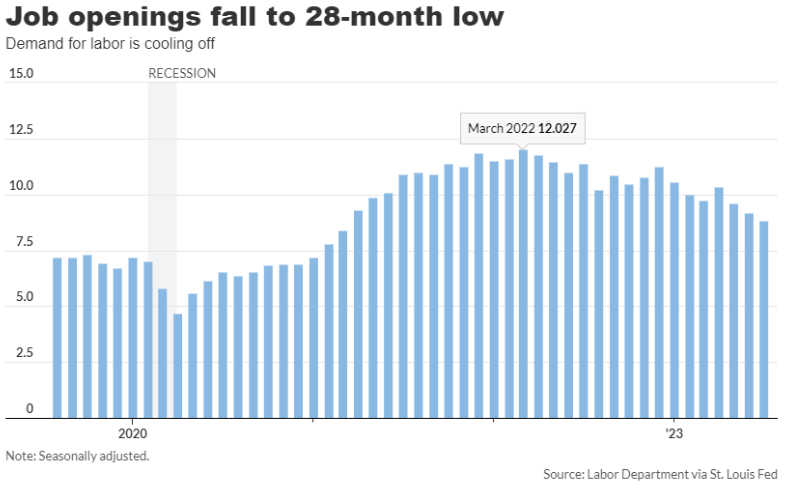

Job Openings (JOLTS), in July, were reported at 8.8M, falling short of the median forecast of 9.5M and June's figure of 9.2M. August ADP employment was at 177K, significantly lower than the forecasted 200K and July's 371K. Both JOLTS and ADP reports indicate a substantial decline in job opportunities.

Data visualized by MarketWatch

The job growth and labor market have now reverted to pre-pandemic levels, alleviating the Fed's pressure to hike policy rates, which in turn supports short-term stock and bond performances. To validate this thesis, the market is keenly awaiting the U.S. nonfarm payrolls, set to be released this Friday. This metric has consistently played a pivotal role in influencing the Fed's policy rate decisions. It is evident that as long as there remains a possibility of multiple interest rate cuts in 2024, even if a deep correction occurs in the short term, a more robust rally can be expected in the future.

While this is positive news for investors, as lower interest rates typically result in increased stock and bond valuations in the short term, the cooling labor market suggests that the economy may be more vulnerable. This should be monitored carefully for its potential implications on long-term strategic asset allocations.

Plowing through Fed Chairman Powell’s Jackson Hole Speech, a rare opportunity to look into his mind for monetary policy decision-making process and his take on the economy, I gleaned two takeaways from the transcript:

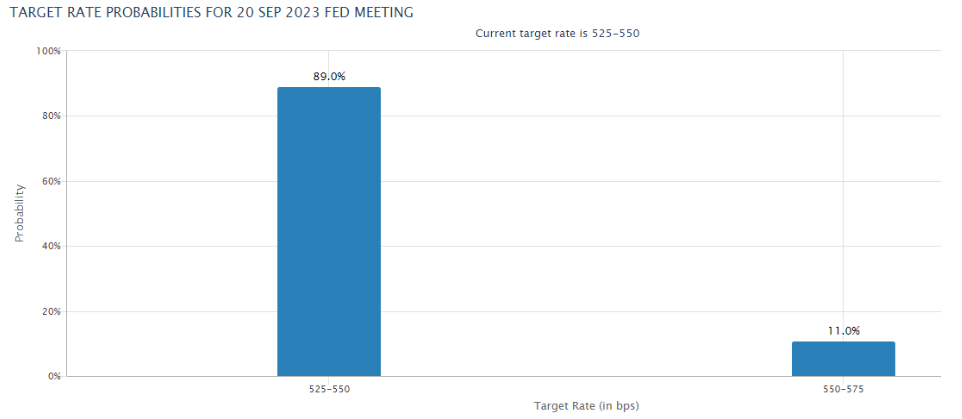

If the inflation risks Powell mentioned materialize, which include a tight labor market driving higher salary inflation, and the lag effect of monetary policies, there's a possibility of future rate hikes exceeding expectations. This hasn't been priced in yet. Currently, the market, indicated by CME, believes there is an 11%(see below) chance of another hike in September, followed by a decline, or at least a plateau, in rates in 2024. If the economy accelerates in the latter half of the year, such changes warrant caution.

Besides inflation and the labor market, it's crucial to closely monitor the central bank's judgment on neutral rates, measuring an economic state that's neither tight nor loose, and it's been a focal point of the Federal Reserve's internal debates recently. This not only affects how high the Feds need to raise rates but also influences future rate cuts and the position of long-term rate levels, significantly impacting investment decisions.

Source: CME

One other important market updates is the potential danger of stagflation in Europe. There are increasing signs showing that the European economy seems to be stagnating. The European inflation data released today shows that the figures for August were 5.3%, higher than the anticipated 5.1%. Moreover, there's no change from the numbers in July, with core inflation also at 5.3%. European headline inflation hasn't shown much variation since June, while core inflation has been hovering above 5% since March. The European Central Bank's interest rate has reached 3.75%, having risen by 75 basis points over the past five months. However, it doesn't seem to have a noticeable impact on curbing inflation. On the other hand, GDP figures aren't encouraging either; the second quarter GDP grew by only 0.3%, which, although above expectations, was primarily driven by France and Ireland. Excluding these two countries, GDP growth was merely 0.04%, virtually stagnant. Given Ireland's status as a tax haven, its GDP growth is somewhat inflated. In contrast, Germany, the locomotive of the European economy, displayed weak performance, with no growth in the second quarter. The Chief Economist of Credit Suisse has commented that Europe has already entered stagnation and won't recover quickly. Traders have already sensed this and have begun shorting the Euro, resulting in almost 5% dip, against USD, since July.

Minutes from the latest European Central Bank(ECB) meeting, date 8/31/2023, also indicate that the risk of Europe entering a stagnation phase is now a concern for the ECB. Hence, to reduce uncertainties, more than mere tightening is required; continued tightening is essential. Before halting interest rate hikes, the committee needs to see clearer signals ensuring that inflation will return to the target.

Stagnation is a central bank's worst nightmare and is equally detrimental for investors. In such scenarios, the entire economic system weakens, unemployment rates spike, and inflation becomes rampant. Implementing traditional measures to stimulate the economy would likely intensify inflation, leading to further damage. On the other hand, refraining from stimulating the economy and allowing it to decline would accentuate issues related to unemployment and consumption issues. This presents a dilemma with no straightforward solutions. The sole successful strategy thus far was embraced by Paul Volcker, Fed’s Chairman and a personal hero of mine, in the 1970s: he opted for a dramatic increase in interest rates, deliberately causing an economic downturn to initially curb inflation before strategizing its revival. Nonetheless, such an approach demands immense courage and would undoubtedly face substantial opposition within the European Parliament(EP). I am skeptical that Christine Lagarde, the ECB President, and Powell's counterpart, could execute such a maneuver, especially when Berlin and Paris have consistently expressed their apprehensions to take measures that could, in their interpretations, jeopardize the European Project. The EU's inherent limitation stems from the fact that it isn't a sovereign nation, meaning its fiscal decisions are made at the member state level, while monetary policy decisions are handled by the ECB. Such a bold move as Volcker's isn't a feasible choice for Lagarde, given she lacks the backing of Germany and France. To be candid, while Shock Therapy was successful for Chile, it led to the downfall of the USSR. I believe adopting Volcker's strategy might not yield success for the EU and could potentially trigger economic calamities due to the aforementioned limitation of the EU. However, if stagflation persists, the EU will find itself devoid of effective solutions. This necessitates our continuous observation and consideration, especially concerning equity and bond exposures in the European markets.

My $0.02

As long as the nonfarm data this Friday and future pertinent statistics back the soft-landing thesis, U.S. stocks, and bonds will set off a strong upward trend in September and hit a new high later this year. Fed's aggressive interest rate hikes in the past have successfully eased the overheated economy, and the labor market will show more signs of cooling, which will prove that the Fed's policy has taken effect. That would also put the Fed on hold for raising rates at its September meeting and potentially lower rates in 2024.

Outside of the US, I believe that policy rates in EM(ex. China) and developed markets(ex. EU) have already been more aggressively done compared to the US and are poised to reap benefits should the US rates start to stabilize and potentially cut rates in 2024.

If I were an asset allocator, I would stick to the positioning I laid out in last month's market observation, which is in economically sensitive stocks that have these traits: 1) leading the recovery in the new economic cycle, 2) possessing strong fundamentals, and 3) either at or near their earnings bottom. The Magnificent 7 tech giants may continue to outperform if their AI productivity boosts to economy thesis holds up, but it's time to start looking at value and non-mega firms. For fixed income, same as last month, I would further extend the duration to lock in today's high yields now that rates are stabilizing and potential cuts could come next year. This would allow capital gains in higher FMVs of bonds when rates get cut.

Palo Alto, CA 8/31/2023

Updates on 9/2/2023

In “My $0.02 section”, my assumption of nonfarm data confirming the validity of the prevalent soft-landing thesis, “giving Fed breathing room on interest rates.”This week’s nonfarm data, together with the JOLTS and ADP data suggest that the economy remains resilient, albeit showing cooling signs and challenges like rising borrowing costs for consumers and businesses. At the upcoming September meeting, the FOMC is highly likely to keep the federal funds rate between 5.25-5.5%. Gargi Chaudhuri of BlackRock mentioned that there's no need for the Fed to be overly aggressive at this time.

While there are still predictions of potential tightening later this year due to concerns on:

1)unpredictable behavior of current economic data,

2)whether more restrictive measures might be needed to achieve the Federal Reserve's inflation target, especially given the resilient consumer spending,

3)specific inflation pockets in certain sectors(not durable goods but in service and housing, according to Powell’s Jackson Hole speech).

I am still confident with my positioning of the markets mentioned above in the“My $0.02 section” based on the aforementioned reasonings and observations unless, later this year, pertinent data depicts an overheated economy and/or exogenous events occur, challenging the soft-landing thesis.